Navigating the rise of female wealth custodians

There have been significant changes over the past few decades with respect to female participation in the workforce and higher education, and indeed in investing. Although females remain under-represented as a whole, they made up half of the 1.2 million net new investors since 2020, according to the most recent ASX Australian Investor Study from June 2023.

These factors may have driven the sharp growth rate in the number of female millionaires, which reached 5.7% in 2023, almost double the growth rate of 3.6% for males according to research The Growth of Women and Wealth by NAB, JBWere, and CoreData.

With women tending to outlive their ageing male partners, the number of female millionaires and their proportion of all millionaires is forecast to continue rising.

Trading data showing marked differences

AUSIEX analysis from late May this year revealed a number of differences between how female and male advised investors have approached their investing over the prior 12 months.

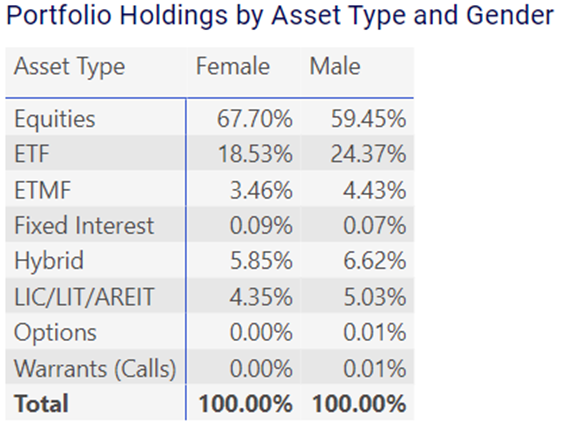

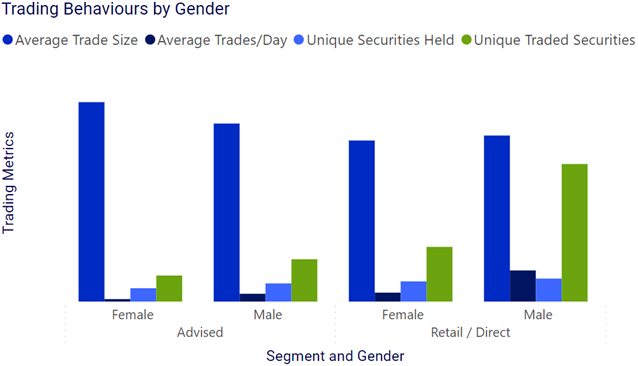

For instance, women in Australia supported by an adviser tend to hold more direct equities than their male advised counterparts, according to AUSIEX data from May this year.

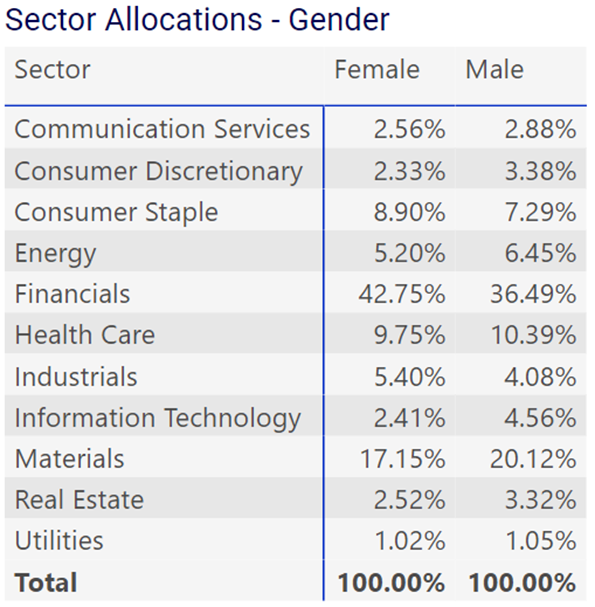

While their actual shareholdings tend to broadly mirror that of men in terms of specific holdings and sector allocations, they hold a greater proportion of consumer staples, financials and industrials compared to their male counterparts, according to AUSIEX data.

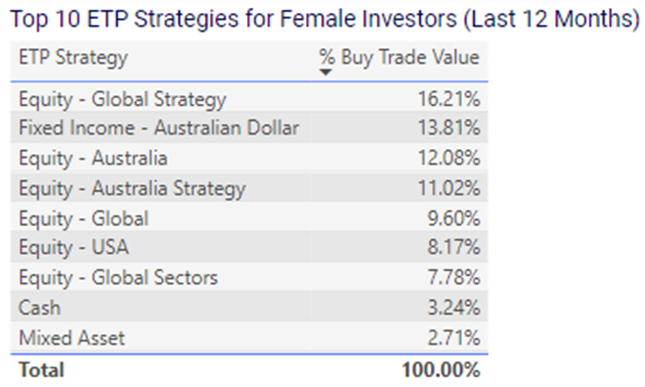

In addition, they tend to also have lower holdings (by value) in exchange traded funds (ETFs). Those that do were buying in the year to May 2024 were buying global equity ETFs, followed by Australian fixed income ETFs and general Australia-focused ETFs.

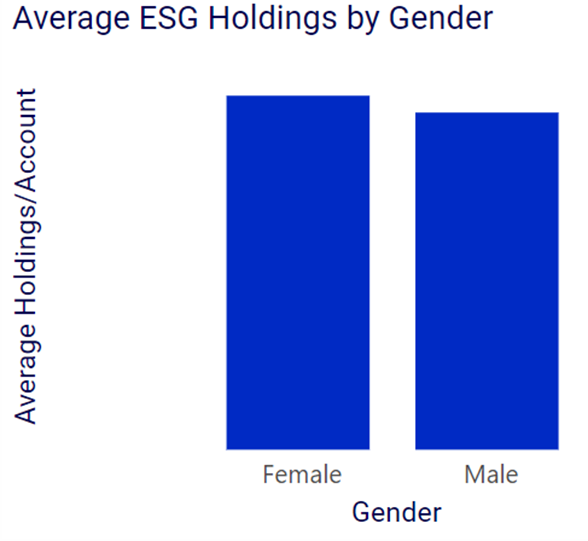

The research also showed that female investors appeared slightly more inclined towards ESG (environmental, social, and governance) investing in their ETF holdings, making this a potential theme through which to engage clients and a consideration when constructing client portfolios.

In terms of diversification, the analysis also found advised female clients held a lower number of unique securities in their portfolios on average than their male counterparts. Portfolios were also more concentrated in single stocks than male accounts, with their largest individual holding comprising a larger proportion of their portfolios value on average.

Source: AUSIEX May 2024

Source: AUSIEX May 2024

Source: AUSIEX May 2024

Source: AUSIEX May 2024

Trading differently, with SMSF interest on the rise

The AUSIEX data also reveals that female investors under advice tend to trade less frequently, but often in larger amounts, compared to male investors. They also tend to trade and hold a slightly smaller pool of securities.

Advised female investors aged 25-49 also had a significantly stronger preference for holdings in ASX20 stocks, with Australia’s largest stocks by market capitalisation comprising 56.94% of portfolio holdings compared with 47.91% for advised male clients (Source: AUSIEX July 2024).

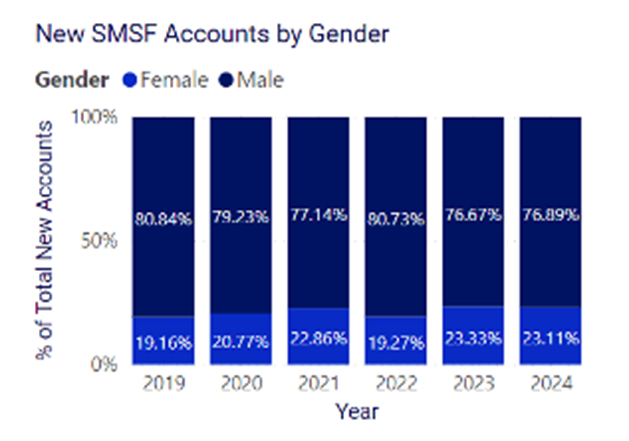

The data also highlights that the proportion of advised female investors with self-managed super funds (SMSFs) is on the rise, as is the gender ratio of new SMSF accounts over the past few years since 2019, as younger female investors seemingly look to take more direct control over their own retirement savings.

Source: AUSIEX May 2024

Source: AUSIEX May 2024

New challenges for advisers as Boomers bust

As the number of male Baby Boomers declines, as they age and pass on, it is important for advisers to recognise that it is not guaranteed that their widows will use the same adviser.

Research from both the UK’s Centre for Economics and Business Research (CEBR) and McKinsey cited in media indicates that nearly 70% of women shed the financial adviser their spouse used within 12 months of becoming widowed. This period is when clients may be most vulnerable and in need of specialist financial guidance.

It is also not just the Boomers which present challenges for the advice industry. Young generations in general it appears, may be less inclined to use their parents’ advisers or even seek financial advice at all. According to research by Cerulli Associates (US), only 19% of affluent investors use the same adviser as their parents, and 92% of investors who use their own adviser did not consider their parent’s adviser in their selection process.

How to capture the opportunities

To address these issues, advisers need to focus on maintaining strong relationships with their clients' families to bridge this gap and ensure continued engagement with younger clientele.

Younger women can also have different investment goals. A recent whitepaper by Fidelity International The Financial Power of Women shows common goals for women include:

- Fully repaying their mortgages

- Contributing to superannuation

- Saving for a comfortable retirement

- Improving financial literacy

- Securing their family's future while building wealth.

Achieving these goals can of course be particularly challenging for women who take career breaks to raise children or care for aging parents.

Advice on how to deal with lower earnings and superannuation balances in comparison with their male counterparts can be topical and important at these life stages. This support would not only help Australian women better manage their finances, but also help set up their future generations to prosper, while also benefiting the practice longer term through client retention.

Stay up to date with the latest insights - sign up to the monthly AXIS email newsletter.

Related Articles