An option to reduce stock volatility

Lewis Taie, Senior Manager Derivatives Program at AUSIEX notes more experienced investors and advisers are considering using options, in particular collar strategies, to provide cost-neutral downside protection.

“No one ever went broke from taking profit” is the old saying, but they may have had to deal with the tax obligation that it created. This is the question some investors are asking regarding their CBA holding given the run over the last 8-12 months.

For investors that have held CBA for more than 12 months, the obligation outlined above may be more palatable given the 50% Capital Gains Tax (CGT) discount (if applicable), though for investors that have acquired CBA within the last 12 months that may not be the case, where hedging some of this exposure through to the 12 month time frame before disposal may be preferable.

If an investor is concerned with the future performance of a stock, such as Commonwealth Bank (CBA), they can hedge their exposure by buying a security with inversely correlated returns, so if the value of your stock goes down, all other things being equal, their hedge should go up.

Investors can potentially achieve this by using futures or warrants with the objective of directly offsetting a loss on a stock.

Alternatively, investors can buy a Put option to lock in a future price for the sale of the stock. Buying a Put has the added benefit of being at the buyer’s discretion, so if the stock remains above the agreed price, the Put will expire worthless with the stock holding remaining unimpacted.

An alternative approach

Each of these strategies, however, has its own pitfall. Futures or warrants will typically provide a like-for-like hedge entirely offsetting any upside, so while you’re hedged to the downside, you’re also not going to see any upside should the stock unexpectedly rally.

With a bought Put, while you keep the upside, the cost of buying the Put can be significant over time, and dependant on how volatile the stock is, potentially cost-prohibitive in practice.

There is a way to use options to obtain the protection of a bought Put without the cost. As with any option position, there’s always a trade-off. In this case, the trade-off comes from funding the purchase of the Put by selling an out of the money Call, effectively foregoing any upside beyond the strike price.

Construction:

For example, consider CBA at 6th June 2025, 3:50PM. (In this case, CBA has been used for information purposes only and this example is not intended to be financial advice.

Stock price was $179.90.

Assuming the investor holds 1,000 shares initially bought in November 2024 @$150.00.

Options Trades:

Buy 10 18th December 2025 Put Strike: $168.00 American (100 shares per contract) @ $5.31

Sell 10 18th December 2025 Call Strike: $190.01 European (100 Shares per contract) @ $5.61

In the above example, the investor has purchased a Put for $5.31, offsetting any share price fall beyond $168.00.

The purchase of the Put is funded by selling a Call for $5.61, where the investor agrees to deliver the stock if called upon at the strike price of $190.01. By writing the Call, the investor limits their potential gain as they will not receive any benefit beyond the $190.01.

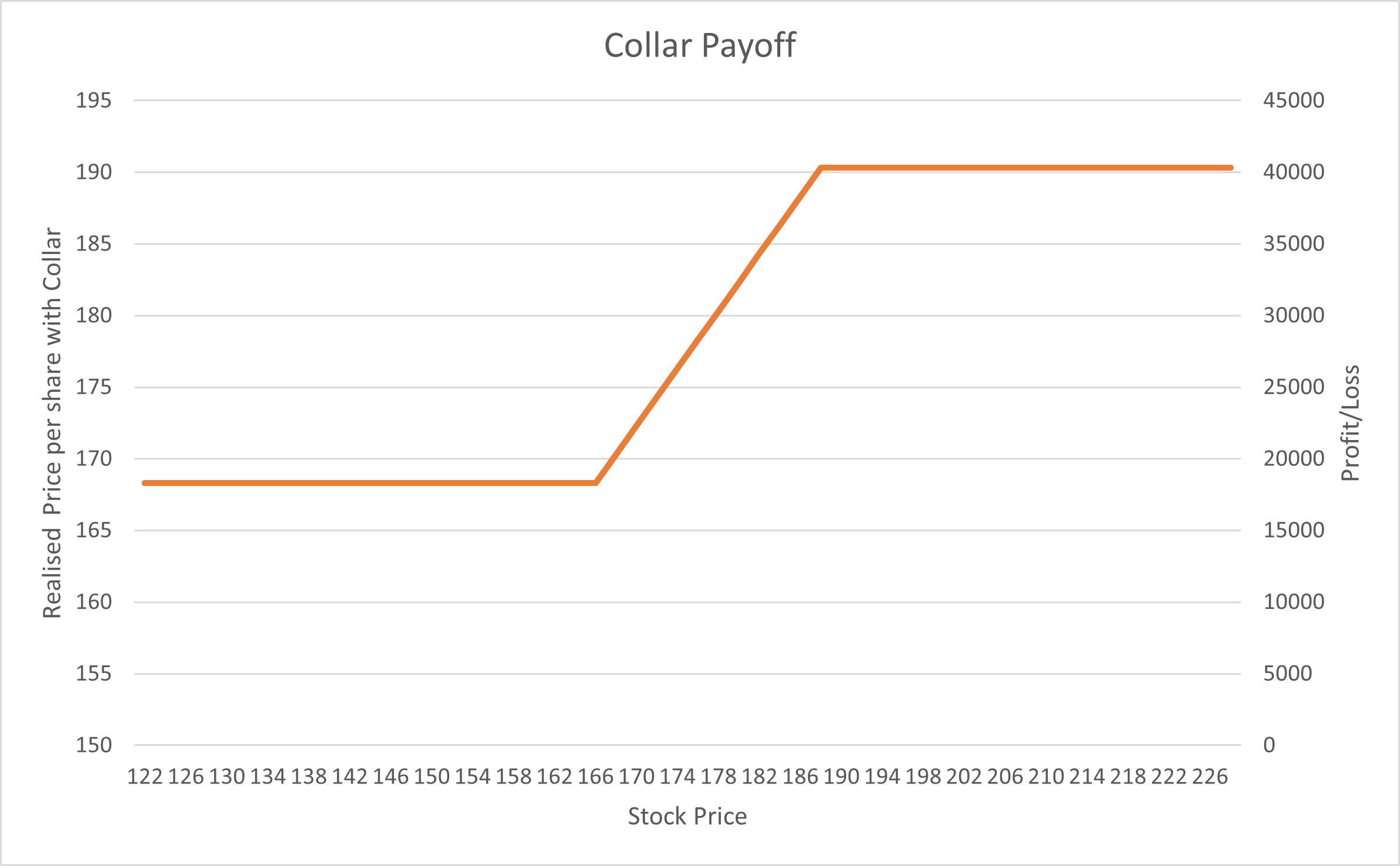

The above example allows the investor to hedge any fall of greater than 6.6% ([168-179.90]/179.90 = -6.6%), at zero cost*, though the investor will give away any further upside beyond 5.6% ([190.01-179.9]/179.9=5.6%), yielding the below pay-off diagram with possible outcomes when the options expire on 18th December.

CBA < $168.00 - Should the price of CBA close below $168.00 per share on 18th December, the sold $190.01 Call would expire worthless, while the bought $168.00 Put would expire in the money and be exercised, allowing the investor to sell their CBA shares at $168.00.

CBA between $168.00-$190.01 - Should the price of CBA close between $168.00-$190.01 per share on 18th December, both the $168.00 Put and $190.01 Call will expire worthless with the investor retaining their CBA shares.

CBA > $190.01 - Should the price of CBA close above $190.01 per share on 18th December, the sold $190.01 Call would expire in the money with the investor assigned and required to deliver their CBA shares at the strike price of $190.01.

The bought $168.00 Put in this scenario would expire worthless. In each case the investor has been able to minimise their exposure to the downside while holding CBA through to 12 months, to be entitled to the 12 month CGT discount (where applicable).

Pitfalls & Considerations:

Downside hedge versus forgone upside

As outlined above, when employing options strategies over a portfolio it’s essential to understand the risk and trade-offs involved and ensure you as an investor are comfortable with them.

When employing a “costless” protective collar for example, it’s important you consider how much of the shares value you are looking to hedge versus what you would be willing to deliver the stock for if it performs strongly.

If you are looking to keep outlay to a minimum (all else held constant), the higher the strike price for your Puts (the more conservative your approach) the more expensive they will be to purchase. This means your Calls will need to have a lower strike to offset the more costly Put hedge. The lower your Call strike price the more upside you potentially forgo should the stock outperform.

Franking

To be entitled to franking credits, the holding period rule requires you to continuously hold shares ‘at risk’ for at least 45 days (90 days for certain preference shares) not counting the day of acquisition or disposal.

For a position to be considered ‘at risk’, you must hold 30% or more of the financial risk. i.e. the delta of the strategy you employ cannot be less than -0.7.

For more information on the tax treatment, you should always engage your accountant or qualified financial adviser.

Writing European versus American

It is worthwhile considering whether to use American or European style options when employing a Collar, particularly on your sold Call. Remembering that American options can be exercised at any time up until expiry while European options can only be exercised at expiry. As it‘s the buyer who has the right to exercise an American style option early, as the seller of the Call (when employing a Collar) we need to consider the likelihood of the counterparty exercising the Call before expiry as this will completely change the strategy and payoff diagram akin to that of a bought Put and may impact 12 month ownership period required for any CGT discount. The example above uses a Sold European Call in order to mitigate this risk.

Summary

Options are often misunderstood, but are simply a tool that when implemented effectively, can allow us to better trade in line with our views.

In this case, a “costless” collar strategy can be deployed when the investor doesn’t wish to sell the stock immediately, though is nervous about potential downside risks coming to fruition and is seeking to hedge some of this risk in exchange for giving away some of the upside should the stock price improve during the life of the option.

* For simplicity, the above examples exclude the small premium generated along with transactions costs, such as brokerage and clearing fees and is considered costless.

AUSIEX provides a leading Exchange Traded Options offering for advisers and institutions. Contact us for more information.

Disclosure / Disclaimer

This information contains general advice and has been prepared without taking into account your objectives, financial situation or needs. You should consider its appropriateness, having regard to your objectives, financial situation and needs. Investors should read the relevant disclosure document and seek professional advice before making any decision based on this information. This information has been prepared by Australian Investment Exchange Limited (“AUSIEX”) ABN 71 076 515 930 AFSL 241400, a wholly owned subsidiary of Nomura Research Institute, Ltd. (“NRI”). AUSIEX is a Market Participant of ASX Limited and Cboe Australia Pty Ltd, a Clearing Participant of ASX Clear Pty Limited and a Settlement Participant of ASX Settlement Pty Limited. Share Trading is a service provided by AUSIEX.

AUSIEX believes the information contained in this article is reliable, however its accuracy, reliability or completeness is not guaranteed and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the Competition and Consumer Act 2010 and the Corporations Act, AUSIEX disclaim all liability to any person relying on the information contained in this article in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information. Persons relying on this information should obtain professional advice relevant to their particular circumstances, needs and investment objectives.

Any opinions or forecasts reflect the judgment and assumptions of AUSIEX and its representatives on the basis of information at the date of publication and may later change without notice. Any projections contained in this article are estimates only and may not be realised in the future. The information is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment.

Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this article is prohibited without obtaining prior written permission from AUSIEX.

Related Articles